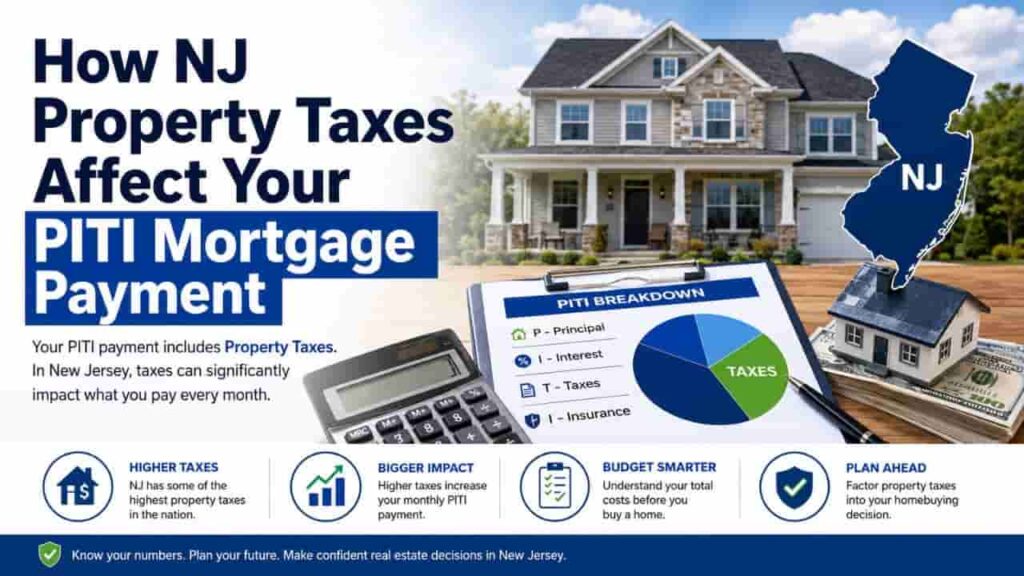

When purchasing a home in New Jersey, looking only at the listing price and the structural mortgage payment can lead to severe financial strain. New Jersey consistently ranks as the state with the highest effective property tax rates in the nation. For first time homebuyers, understanding how these real estate taxes integrate into a monthly housing budget is critical. Your true monthly housing expense is not just the principal and interest on your loan. It is structured as PITI, which stands for Principal, Interest, Taxes, and Insurance. Because New Jersey’s localized tax rates significantly inflate the “T” in PITI, failing to accurately calculate this component can distort your debt to income (DTI) ratio and disrupt your homeownership plans.

The Breakdown of a PITI Mortgage Payment

To properly budget for a home in the Garden State, buyers must understand how lenders calculate the four distinct components of a standard monthly mortgage payment.

[ Monthly Mortgage Payment (PITI) ]

P. Principal (Loan Balance)

I. Interest (Lender Fee)

T. Taxes (NJ Property Tax)

I. Insurance (Homeowners + PMI)Principal and Interest (P&I)

The core of your mortgage payment consists of the principal the actual dollar amount borrowed from your financial institution and the interest, which is the fee the lender charges you for borrowing those funds. These two numbers are determined by your total loan amount, your credit score, and current macroeconomic market rates.

Taxes (T)

This represents your municipal property tax allocation. In New Jersey, property taxes are assessed locally by individual townships and counties to fund public school districts, municipal infrastructure, and county services. This single variable introduces the most volatility into an NJ housing payment.

Insurance (I)

This includes your standard homeowners hazard insurance policy, which protects the physical structure from damage. Additionally, if your down payment is less than 20% on a conventional loan, this component will include Private Mortgage Insurance (PMI), a monthly premium that protects the loan servicer in the event of default.

How the Escrow Account Handles NJ Property Taxes

Lenders do not want to risk a municipality placing a tax lien on a property they finance. To prevent this, most structural loan agreements require the establishment of an Escrow Account. An escrow account acts as a dedicated holding fund managed directly by your Loan Servicer. Instead of paying your massive property tax bill directly to the local township tax collector every quarter, your servicer breaks the annual tax bill into twelve equal parts and adds it directly to your monthly PITI statement.

| Payment Flow Step | Responsible Party | Operational Action |

| 1. Collection | Homeowner / Borrower | Pays 1/12th of the annual property tax and insurance premiums as part of the monthly PITI payment. |

| 2. Accumulation | Loan Servicer | Holds the tax portion in a non interest bearing escrow account until the municipal payment deadline approaches. |

| 3. Disbursement | Loan Servicer | Disburses the funds directly to the local NJ municipal tax collector on the standard quarterly due dates. |

The Danger of the NJ Escrow Shortage

Property tax rates across New Jersey’s 564 municipalities are not static. Local school boards vote on new budgets, and townships undergo comprehensive municipal revaluations. When these structural tax shifts occur, your monthly mortgage setup experiences a significant disruption known as an Escrow Shortage.

Why Escrow Shortages Occur

Every year, your loan servicer conducts a mandatory Escrow Account Analysis. They look at the current balance of the account, project the upcoming year’s property tax liabilities, and compare it against the current collection rate. If your local township raises its tax rate mid year, your servicer will have disbursed more money to the tax collector than they collected from you. This creates a retroactive deficit.

The Double Impact on Monthly Payments

When an escrow analysis identifies a shortage in a high tax state like New Jersey, the homeowner faces a compounding financial adjustment. The loan servicer will adjust your monthly payment in two ways.

- They collect the retroactive shortage amount over the next 12 months.

- They increase the forward looking “T” portion of your PITI payment to match the higher tax rate.

This adjustment can cause a sudden, unexpected increase of several hundred dollars in a homeowner’s monthly housing costs.

Visualizing PITI, A Practical New Jersey Example

To illustrate how dramatically property taxes affect affordability, let us look at a practical purchasing scenario. Consider a home bought for $500,000 using a standard conventional loan with a 10% down payment ($450,000 loan amount) at a fixed interest rate. We will compare a typical New Jersey municipal tax profile against a standard national average profile.

| Cost Component | National Average Tax Profile (1.1%) | High Tax NJ Municipal Profile (2.6%) |

| Principal & Interest (P&I) | $2,844 / month | $2,844 / month |

| Property Taxes (T) | $458 / month ($5,500/year) | $1,083 / month ($13,000/year) |

| Homeowners Insurance (I) | $125 / month | $125 / month |

| Private Mortgage Insurance (PMI) | $95 / month | $95 / month |

| Total Monthly PITI Payment | $3,522 / month | $4,147 / month |

The Affordability Gap

As demonstrated above, buying the exact same house with the exact same loan parameters costs an additional $625 every single month in New Jersey purely due to the local property tax rate. This structural difference requires a homebuyer to earn significantly more annual income to pass standard lender underwriting ratios for the same purchase price.

Step by Step Guide to Proactively Managing Your PITI

To avoid payment shocks and manage the complexities of New Jersey housing costs, implement this step by step financial management strategy.

Step 1. Research the Specific Municipal Tax Rate

Do not rely on the historical property tax numbers listed on public real estate portals, as they are often outdated. Visit the official County Board of Taxation portal or review the property’s asset profile using the local tax assessor’s data to find the exact current effective tax rate.

Step 2. Factor in Potential PMI Costs

If you are putting down less than 20%, request an itemized quote from your loan officer detailing your exact monthly PMI premium. Ensure this figure is accounted for within the insurance quadrant of your PITI calculation.

Step 3. Use an Accurate Mortgage Calculator

Before making an offer on a home, input the specific municipal tax rate, estimated homeowners insurance, and PMI data into a localized PITI Calculator. This ensures you are viewing your true monthly liability rather than an idealized estimate.

Step 4. Monitor Local Municipal Budgets

Pay close attention to local school board elections and municipal budgeting sessions in your township. If a school bond referendum passes, anticipate the tax increase and begin budgeting for the subsequent escrow account adjustment before your servicer runs their annual analysis.

Conclusion

Understanding homeownership in New Jersey requires moving beyond simple listing prices and analyzing the structural realities of PITI payments. The state’s unique property tax infrastructure means that your loan servicer and escrow account play an outsized role in your ongoing monthly financial stability. By proactively calculating true tax liabilities, preparing for potential escrow shortages, and accounting for variables like PMI, buyers can safeguard their household budgets against unexpected payment increases and secure long term housing affordability.

FAQs

What does PITI stand for in a mortgage payment?

PITI stands for Principal, Interest, Taxes, and Insurance, representing the four comprehensive components that make up a homeowner’s total monthly housing payment.

Why are property taxes collected in an escrow account?

Loan servicers mandate escrow accounts to ensure municipal property taxes are paid on time, protecting the lender from costly local government tax liens.

How does an escrow shortage affect my monthly NJ mortgage?

An escrow shortage requires your loan servicer to increase your monthly payment to recover the past deficit while simultaneously adjusting for higher future tax rates.

What is Private Mortgage Insurance (PMI) within PITI?

PMI is a monthly premium required by conventional loan servicers when a homebuyer provides a down payment of less than 20% of the purchase price.

Can I pay my New Jersey property taxes directly instead of using escrow?

Some lenders allow direct payments if you put down 20% or more, but they may charge a waiver fee and require proof of structural compliance.

How often do loan servicers analyze my escrow account balance?

Federal regulations require loan servicers to perform an official Escrow Account Analysis at least once every 12 months to verify payment accuracy.

Do New Jersey home renovations impact my monthly PITI payment?

Yes. Capital improvements can trigger a municipal added assessment, which increases your property’s assessed value and subsequently raises the tax portion of your PITI.