In New Jersey, your property tax bill is a product of two numbers, the local tax rate and your property’s assessed value. While you cannot easily change the tax rate, you have a legal right to challenge an unfair assessment. With the 2026 tax year now in full swing, many homeowners are noticing that their assessments don’t align with the current cooling market trends. This professional guide provides a technical roadmap to filing a successful appeal, applying the Chapter 123 Ratio, and meeting the strict April 1st and May 1st deadlines.

The Foundation of a Tax Appeal Market Value vs Assessment

A tax appeal is not a complaint about “high taxes.” Legally, it is a challenge to the valuation of your property. To win, you must prove that the assessed value assigned by the municipal assessor is higher than the true market value of your home as of the statutory valuation date. October 1st of the pre tax year.

Understanding the Chapter 123 “Fairness” Test

New Jersey uses a formula known as Chapter 123 to determine if your assessment is equitable. Since most towns do not assess at 100% of market value every year, the state publishes a Common Level Range.

| Scenario | Calculation Result | Outcome |

| Below Lower Limit | Your ratio is significantly low. | The state may actually increase your assessment. |

| Within Range | Your ratio is within 15% of the average. | No change is permitted; the assessment is “fair.” |

| Above Upper Limit | Your ratio exceeds the average by 15%+. | Mandatory Reduction to the Common Level. |

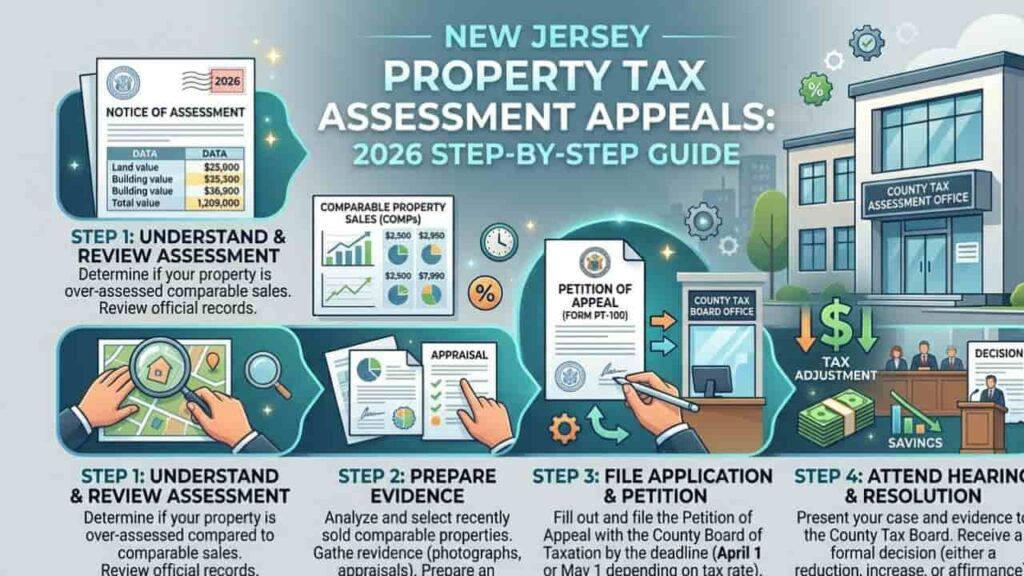

Step 1. Critical 2026 Deadlines and Notifications

Your journey begins with the Notice of Assessment postcard (usually green or white) mailed in late January or February 2026. This card lists your new assessment and the specific deadline for your municipality.

2026 Filing Deadlines by County

Missing these deadlines by even one day results in an automatic dismissal of your case.

- April 1, 2026

The standard deadline for the vast majority of New Jersey municipalities. - May 1, 2026

Standard deadline for Bergen County residents and any municipality (like those in Monmouth or Ocean) that underwent a full municipal wide revaluation or reassessment for 2026. - December 1, 2026

Deadline specifically for Added or Omitted Assessments (usually for new construction or major renovations completed mid year).

Step 2. Gathering “Usable” Evidence

The County Board of Taxation will not accept photos of a leaky roof or a noisy neighbor as primary evidence. You must provide Comparable Sales (Comps) that occurred near the October 1, 2025 valuation date.

What Makes a Sale “Usable”?

- Arms Length Transactions

The sale must be between a willing buyer and seller (no foreclosures, short sales, or family transfers). - Proximity

Ideally, the homes should be in your neighborhood or a similar part of town.

Professional Tip. You must submit your list of comparable sales to the Tax Board and the Municipal Assessor at least 7 days prior to your scheduled hearing.

Step 3. Filing the Appeal (Form A-1 vs Tax Court)

Depending on your home’s value, you will choose between two paths.

County Board of Taxation (Form A-1)

This is the standard path for most residential properties (Class 2). You file with your specific county board (e.g., Essex, Morris, or Passaic). The process is relatively informal and often handled by homeowners without an attorney.

NJ Tax Court

If your property’s total assessment exceeds $1,000,000, you have the legal right to bypass the County Board and appeal directly to the State Tax Court.

2026 Filing Fees (County Board)

| Assessed Value | Filing Fee |

| Under $150,000 | $5.00 |

| $150,001 – $500,000 | $25.00 |

| $500,001 – $1,000,000 | $100.00 |

| Over $1,000,000 | $150.00 |

Step 4. The Hearing and Decision

Most hearings for the 2026 cycle will take place between May and July. During the hearing, you will present your evidence to a Tax Commissioner.

- The Assessor’s Role

The municipal assessor will also present evidence to support their valuation. - The Burden of Proof

As the appellant, the burden is on you to prove the assessment is wrong. If the evidence is a “tie,” the original assessment stands. - The Judgment

You will receive a written “Judgment” via mail (usually a Memorandum of Judgment) within 45 days of the hearing.

Common Pitfalls that Lead to Dismissal

- Late Filing

Even if the postmark is the deadline date, the Board must receive the paper form by the deadline (unless using an authorized online portal). - Unpaid Taxes

You cannot appeal your assessment if your property taxes or municipal charges (water/sewer) are in arrears for the current or prior year. - Hearsay Evidence

You cannot simply say “Zillow says my house is worth $X.” You must provide the actual sales data (Deed Book/Page) for your comps.

Summary of Taking Control of Your Tax Bill

Appealing your property tax assessment is a vital tool for New Jersey homeowners to ensure they aren’t subsidizing the rest of the town. By identifying your Common Level Ratio, gathering at least three solid comparable sales, and filing Form A 1 before the April 1st (or May 1st) deadline, you can successfully align your tax burden with the true market reality of 2026.

Conclusion

A successful 2026 NJ tax appeal hinges on meeting the April 1st or May 1st deadlines with undeniable market evidence. By leveraging comparable sales and understanding the Chapter 123 fairness formula, homeowners can effectively dispute over assessments. Don’t let an inaccurate valuation inflate your tax bill file Form A 1 early and protect your home’s equity.

FAQs

Will an appeal increase my taxes?

It is rare, but possible. If the Chapter 123 test shows you are severely under assessed (below the Lower Limit), the Board has the authority to increase your assessment to the Common Level.

Do I need to hire a professional appraiser?

For residential appeals, you can often act as your own expert by providing sales data. However, for high value homes or complex properties, a licensed appraiser’s testimony is much more persuasive to the Board.

Can I appeal my taxes because the town services are poor?

No. Poor road conditions or school issues are budget matters handled at town council meetings. The Tax Board only has the jurisdiction to change the valuation of the property.

How long does a successful appeal last?

Under the Freeze Act (N.J.S.A. 54:3-26), a successful judgment is typically protected for the year of the appeal and the two following years, unless the town undergoes a municipal wide revaluation.

What if I am unhappy with the County Board’s decision?

You have 45 days from the date the Judgment was mailed to file an appeal of that decision with the NJ Tax Court.